Good credit pays off. Even if you’re not planning to borrow money to make a large purchase, good credit may qualify you for better insurance rates, help you avoid paying security deposits when you sign up for new cell phone service or even help you negotiate a better rate on a vacation rental.

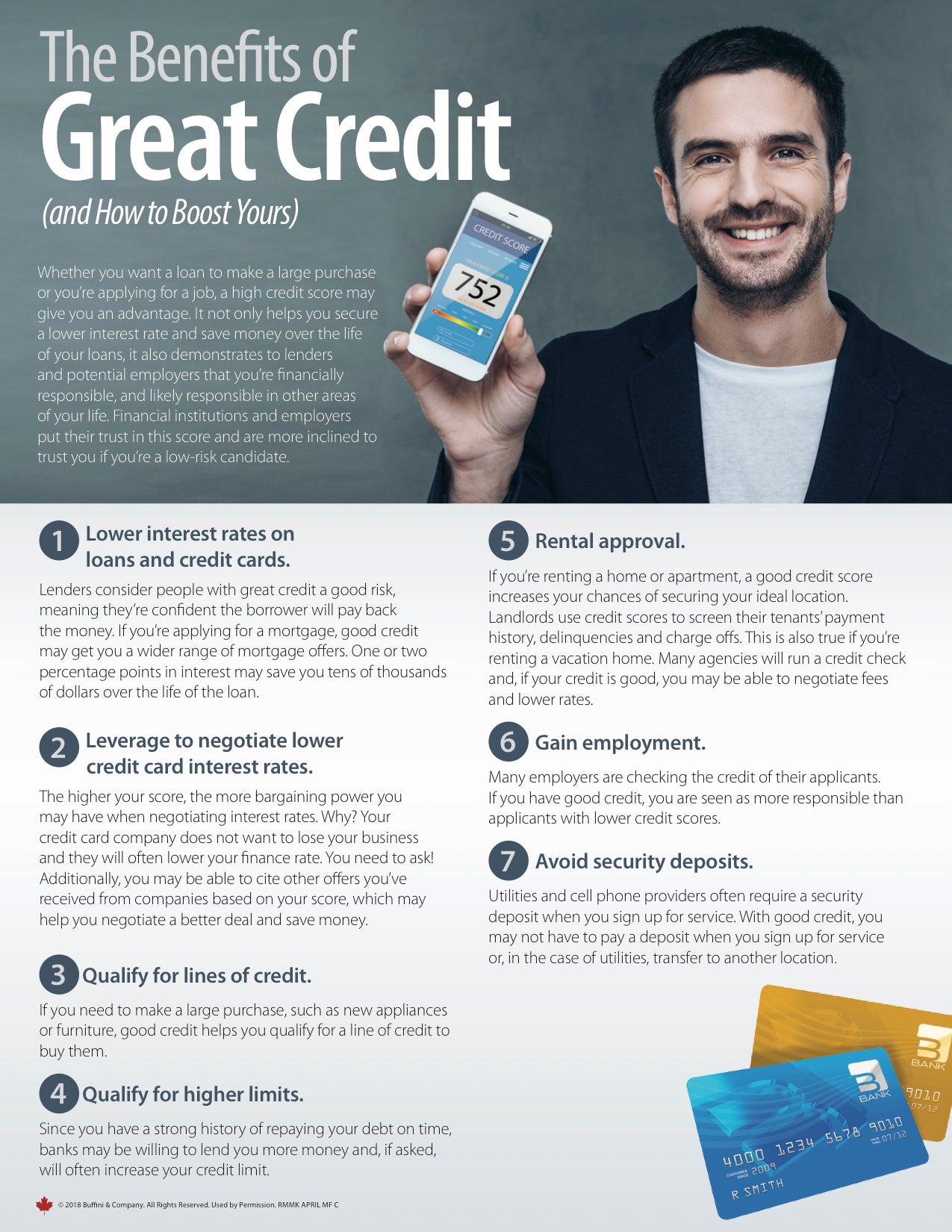

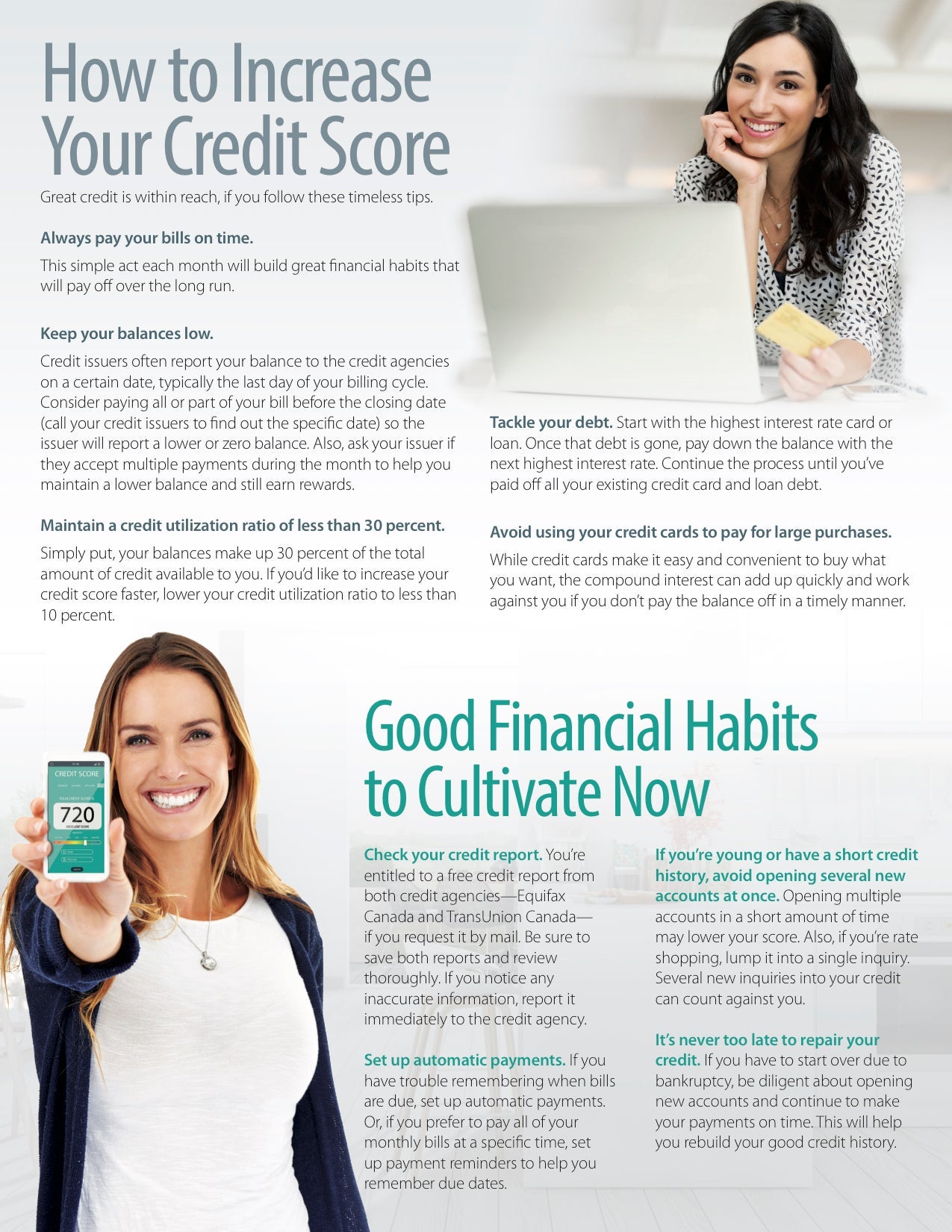

The information I’m sending this month not only outlines some of the benefits of great credit, it also provides ways to improve it. Page one delves into seven benefits of having good credit, from qualifying for lower interest rates on loans and credit cards to improving your chances of getting a great job. Page two provides five tips to help you improve your credit score. If your credit is already great, the tips will help you ensure it remains high.

If your credit is already stellar, feel free to pass this information along to someone else who may benefit. This information is intended to help make financial goals more achievable.

☞ Here is some excellent advise from a Colleague of mine Tara Borle, Lead Mortgage Planner with Mortgage Architects.

Thank you Peter for asking me for my input on credit bureaus. As a mortgage broker I look at credit on all mortgage applications. A lot of people don't understand the importance of credit bureaus when applying for any type of credit.

When you apply for new credit the bank will review your credit bureau to see how you pay back your existing credit. They are also looking to see if you’ve missed any payments, how much money you have owing to creditors and if you are at near the limits of your credit cards and lines of credit.

To ensure you receive the best rate and conditions on a credit approval – it’s important to pay all existing credit on time and to keep enquires on your credit to a minimum. Each check or enquiry does lower your credit score.

To continue to ensure you have good credit – always pay the minimum required by the bank before the due date on the statements you receive. It is normal to have a few enquires per year on your credit bureau. If there has been a reason for late pre-payment on credit and a reasonable explanation – for example, an injury or a mix up on an account I can provide an explanation on your behalf.

What do you do if you have a low credit score? There are ways to rebuild your credit or establish credit, you can obtain a secured credit card or get an rsp loan from a bank. Both of these credit facilities report on your credit bureau which will build your score. Even if you can pay your rsp loan off, what you want to do is make the loan payment every month on time so that it reflects that you have continually made payments.

To review your own credit bureau you can do that by going to equifax.ca. It is a good idea to check your own credit periodically to ensure there are no creditors reporting that shouldn’t and that there are no errors on your bureau.

Please feel to contact Tara with any mortgage questions you may have.

Tara Borle

Lead Mortgage PlannerMortgage Architects

c: 780-237-7653

f:780-669-7193